OneCity Insights

Why we are building OneCity

Creating digital tools to make land markets transparent and urban plans work

We aspire for a future where property entrepreneurs are equally empowered with real-time market data, up-to-date regulatory knowledge, and insights into the impacts their projects may have on the community and environment.

The Challenge: Property Developer

A property entrepreneur has hundreds of hurdles to jump before converting a derelict building or an empty plot of land into a successful venture. Some hurdles are predictable, and some are unique. And how a developer resolves them can make the difference between bankruptcy or a successful investment. For OneCity Insights, we focus on the first step in the development process: finding the right investment opportunity. Choosing the right plot of land or property is a critical decision.

[The] information about land is not readily available to the public. […] So if you don’t know you might waste money. So this to me is very crucial to know.

Deon Van Zyl — WCDF

The Challenge: City and Community

The problem of affordable housing, accessible public transport and urban sprawl in South Africa are well known. While there are great efforts to build new housing, much of it is spread out in areas far from city centres. This means many South Africans live far from where they work.

City planners have developed strategies to overcome these challenges. However, rapid population growth and inefficiencies in land markets, public funding and delivery result in deepening problems. The greater the urban sprawl, the more infrastructure and public funding will be needed in the future. Urban sprawl cannot be undone once it has occurred, and the moment to tackle it is now.

OneCity Insights helps to find profitable investment opportunities that comply with planning regulations and are near services and jobs. This makes cities and communities more equitable and resilient.

How do we do it?

In this release of OneCity Insights, we identify opportunities across the City of Johannesburg to develop single-family detached houses that fit the current property market climate.

To identify these opportunities, we go through 4 stages: we decide on Typology, filter out sites that do not fit our purpose or with high risks, then sort development opportunities from the best to the worst, and, finally, add property market data for each site.

In detail, these stages (Fig. 01) include:

Step 1. Deciding on Property and Site Typology

Filtering Opportunities by

Step 2. Land Use Rights

Step 3. Size and Shape

Step 4. Planning Risks

Step 5. Potential Development Coverage

Sorting Opportunities by

Step 6. Planning Risks and Incentives

Step 7. Development Impact

Step 8. Potential Development Coverage

Calculating additional Insights

Step 9. Property Markets

We identified 181 753 opportunities in Johannesburg to develop or extend single-family detached houses that fit the present property market climate. 2 452, which is 1.5% of these opportunities, have high development potential and are close to amenities and public transport.

Step 1. Property and Site Typology

At this stage, we are looking exclusively into single-family detached housing developments in Gauteng. When this type of housing is mixed with services at the proper density it creates a quality urban environment and strong communities.

Even though Gauteng is the smallest province in South Africa by land area, it is one of the two largest property markets (along with the Western Cape). More than 3,000 detached single-family houses were built here in 2021 alone, making this market segment larger than flats and townhouses by value.

We have evaluated more than 200 single-family development projects in Johannesburg and Pretoria to identify the most sought-after housing typology. The results provide a wide range of development opportunities varying in parcel dimensions, floor size, and the number of bedrooms. See identified typologies in Fig.02.

Type SDU:

Subsidiary Dwelling Unit (SDU) development is a popular model for many property owners in CoJ. The latest town planning regulation allows an owner of a property zoned Residential 1 to build up to two subsidiary dwelling units on the said property. Of course, subject to additional conditions, it is an opportunity for small-scale developers which simultaneously stimulates the densification and diversification of low-density residential areas.The floor area of the subsidiary dwelling units cannot exceed 160m² or 90% of the main dwelling house. The overall development should also comply with the density and the site coverage criteria attributed to the area. These units may only be built in relation to an existing dwelling. By following these guidelines, property owners can expand a home or create an additional rental unit while staying within the parameters set by planning rules.

It is vital to remember that the choice of typology creates a particular density *, diversity and sense of place. The higher density and diversity, the more of a ‘centre’ an area becomes and the more services and intercity transport are required. Lower densities with no services and jobs around make residents depend on cars or extensive public transport routes. It makes living expensive and the city less healthy.

* Land and Use Scheme Guidelines 2017 by the Department of Rural Development and Land Reform define the above typologies as Medium density for Type S, Low Density for Type M, and Very Low Density for Type L. It recommends which urban areas should accommodate these densities to achieve a balanced and fair city.

Despite these guidelines and the corresponding CoJ Land Use Scheme 2018, Johannesburg faces a lot of pressure from property developers to build on the urban periphery. Township establishments and re-zoning on the periphery feed urban sprawl and transport mobility problems.

Conversely, mixed-use areas with diverse housing typologies and densities, balanced with public transport infrastructure and services, create more advantageous environments.

In OneCity Insights, we use additional tools (like Development Impact Gauge) to the planning regulations to identify investment opportunities in locations that are favourable for the city and sought-after by leading investors.

Step 2. Land Use Rights

Residential property can only be built on land that has corresponding ‘Residential’ Land Use Rights according to the Land Use Scheme*. These ‘Residential’ Land Use Rights could be Primary and Secondary and include dwelling houses, dwelling units and residential buildings. If future development matches Primary Land Use Rights (e.g. you are planning to build a detached house on land with Primary Land Use Rights that include dwelling houses) the process to obtain the permission is easy. You only need to submit a Building Plan making sure it complies with set restrictions for density, height, setback and more.

In contrast, if your future development is permitted only according to Secondary Land Use Rights, you must submit a Land Use Management Application and go through the rezoning process. The rezoning process is long and painful and, most importantly, requires the relevant land to be purchased by the applicant beforehand. The latter is a substantial barrier for smaller entrepreneurs.

By identifying developable sites that do not require rezoning, we want to unlock development opportunities that are suitable for smaller entrepreneurs, in a market dominated by large developers.

The good news is that residential property is automatically permitted as Primary Land Use Rights in 7 Zones: Residential 1–5 and Business 1–2.

*What is a Land Use Scheme (LUS)?

A Land Use Scheme is a set of rules for a given city that determines which uses are allowed for specific pieces of land in the city. The list includes everything from residential to commercial and industrial zones, with each zone having specific purposes assigned by law — meaning you cannot just start building anything anywhere. A Land Use Scheme not only sets out the various uses of land and buildings in a city but also lists what you can do with each category of land. For example: if your house needs more space and is in a Residential 1 area permitting a Subsidiary Dwelling Unit, you can extend your property without any Land Management Application — all you need is a Building Plan that complies with rules for Subsidiary Dwelling Units. However, in cases where an application needs to be made, you should carefully consider the provisions of the relevant Land Use Scheme and SPLUMA together with the Spatial Development Framework, Municipal By-laws and other documents before preparing any land management applications.

How do we find land with Primary Rights that fit our purpose?

There are a total of 652 974 sites with Primary Land Use rights that fit the housing typologies we seek to build. However, not all of them are actually legitimate.

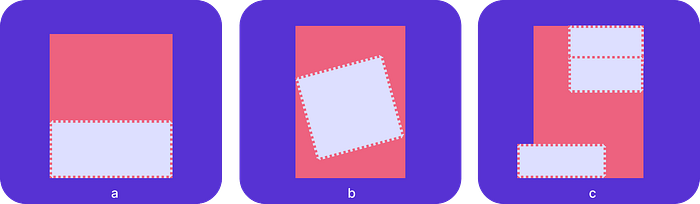

By looking more closely at the identified sites, we found that some of them overlap. There are some larger plots divided into two (or more) smaller ones (fig. 04a). Thus, you have several small erven and a larger one that covers them all. Then there are those partially overlapping, meaning the erven are of different shapes or positions and one part is overlapping (fig. 04b). There are also cases with multiple overlapping plots (fig. 04c). What is wrong with these sites and how to know which are legitimate ones to consider?

By looking deeper into the attributes of the sites, we found that overlapping plots have different subdivision statuses — either a Registered Stand, SG Approved Stand or Proclaimed Township.

Registered Stands are the plots that are registered in the Deeds Office and have information on zone restrictions (e.g. height, density, coverage, etc.) SG Approved Stands and Proclaimed Townships are the ones not registered in the Deeds Office. To consider these, one needs to find out from the Deeds Office why the property is not registered. There are usually multiple reasons.

To be sure that one will not have problems with future development, we decided to consider Registered Stands only, meaning those registered in the Deeds Office — the main organisation that manages property rights

By filtering out unregistered sites and keeping only those registered with the Deeds Office, we reduced the number of sites that fit our purpose from 652 974 to exactly 601 479 plots, which is 92% of the original total.

Total of residential sites: 601 479 plots, which is 92% of the original total.

Step 3. Size and Shape

What plot sizes are we after?

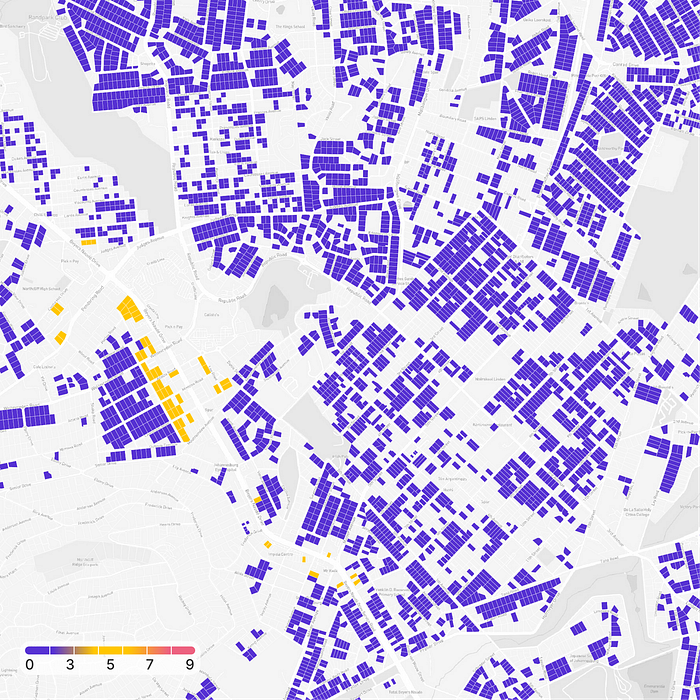

In the market analysis, we identified housing typologies that correspond to the erven range of 300 to 800 m2. At this point, we decided to limit the maximum size of the plot to 2000 m2. It means that once the internal access roads are built (or setback lines are accounted for) the 2000 m2 could accommodate up to 2 units of the typology L or up to 6 units of the typology S. By limiting our search to this range we identified 423 093 sites (Fig. 05) in Joburg (65% of the original total).

Why do plot shapes matter?

The shape of your land plot can significantly impact the feasibility and cost of future development. The perfect land plot requires minimum investment into it and, when developed, creates a well-positioned product for the market. Irregularly shaped land plots impose multiple restrictions on the position of the building and require additional site infrastructure. Particularly for smaller parcels, the shape of the site can impose restrictions on the shape and efficiency of the building itself. Parcel Shape Index (PSI)* is one way to measure how well-suited a parcel is for development (Fig. 06).

* We use two metrics to measure the shape of parcels (PSI): compactness and regularity:

Compactness shows how far a land plot deviates from the most efficient shape — a circle. It calculates the ratio of the circumference of the equivalent circle to an actual perimeter of a land parcel.

Regularity shows how close it is to a perfect rectangle. It calculates the ratio of the smallest possible bounding rectangle area with a parcel area.

In both metrics, the closer a metric is to “1”, the closer a site is to a perfect shape, i.e. the more compact and regular the parcel is. The resulting PSI identifies less risky and more profitable development opportunities.

By applying a PSI value of 0.8, we limit the number of sites having significantly higher development potential to 376 575 which is 58% of our original total.

Total of residential sites: 376 575, which is 58% of the original total.

Step 4. Planning Risks

To decide on a new project, a developer needs to diligently check all of the risks, details and constraints associated with a property. Some of these checks are only possible on-site (e.g. technical surveys) and require a permit. Yet much information can be found in public registers. For example, the Land Use Scheme 2018 contains some of the most basic and important details.

We analysed Risks & Constraints available in public registers, and explain what they mean and their importance for our development typologies (Fig. 07). Finally, we make our Importance Verdict.

A score of 5 means no development is possible; these sites are excluded completely. Scores of 0 to 4 mean no to high risk; these sites receive grades from 0 to 4, which are subtracted from a base development potential of 0. As an example, a site located in the Dolomitic Area will have a development Potential of 0–3=-3.

Explore Risks and Constraints in detail (Fig. 08).

Total of residential sites: 323 994, which is 50% of the total.

Step 5. Potential Development Coverage

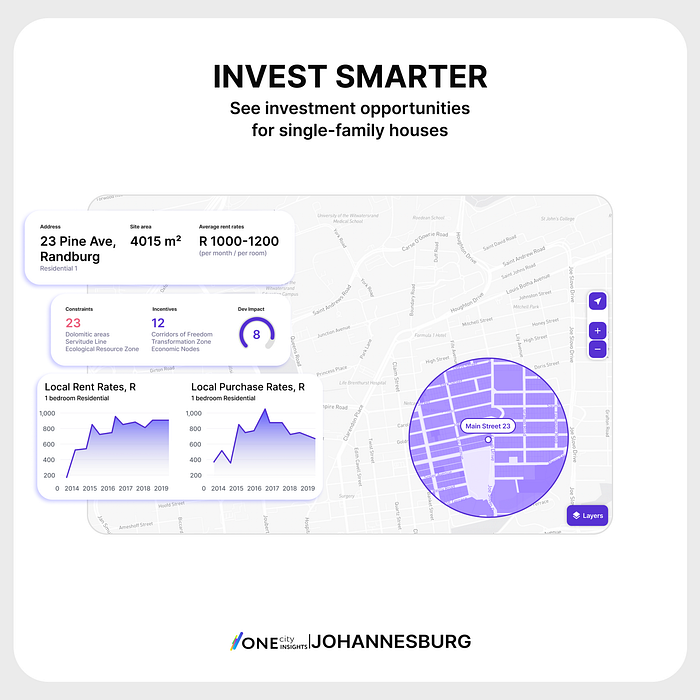

We use image recognition technology and machine learning to calculate the development potential of each land plot. Together with market data, this gives an entrepreneur intelligence into what return on investment can be achieved.

How do we calculate Potential Development Coverage?

The sites with potential development coverage are the ones that have actual built-up area coverage lower than the coverage permitted by the Land Use Scheme (in case of consent use) or Nodal Review 2019/20 and SDF 2040 (in case of rezoning). To calculate potential development coverage, we compared the existing built-up area (coverage) with the coverage area permitted by the planning documents.

Important note about data and accuracy*.

* We use two datasets to calculate potential development coverage: building footprints provided by CoJ (available at GeoLIS) and Microsoft Building Footprints.

The GeoLIS dataset provides great accuracy but has these limitations:

- Coverage. The dataset covers 24% of the CoJ including Randburg, Roodepoort, Sandton, Midrand, Baralink, and Jabulani and several priority zones (i.e. CBD and area along railway and BRT routes).

- Validity. The dataset is dated back to 2012. Therefore any development built after that is not recorded.

Microsoft Building Footprints is an AI-based dataset. It is nationwide in scale and is up-to-date (the latest dataset is based on satellite imagery of 2020 and 2021). Microsoft states that the model for Africa matches buildings with a precision of 64.5%. To maximise the accuracy, we cross-check these datasets.

However, we advise seeking more precise information (e.g. zoning certificate and on-site survey) on any particular property or site before making any decisions.

Please refer to our Disclaimer.

By running the above calculations (Fig. 09) we identified 181 753 sites that have potential development coverage. This figure includes sites with moderate potential development coverage, usually an extension to the existing building’s coverage area of 30–50%. For the sites where the coverage could be increased by more than 50% the development potential is high, this could be a Subsidiary Dwelling Unit on Residential 1 or additional property in other zones. You can find the potential development coverage in square meters for selected sites in any given location at OneCity Insights.

Total of residential sites: 181 753, which is 28% of the total.

Step 6. Planning Risks and Incentives

We sort sites in OneCity Insights Report by Planning Constraints and Development Incentives (we use combined rating), Development Impact and Potential Development Coverage.

We sort in the following order:

- By combined value of Constraints (from none to maximum) and Incentives (from maximum to none);

- By Development Impact value, from the great to none;

- By Potential Development Coverage value, from the max to min.

In short, you get a list of development opportunities in the order of priority — first are the sites with minimum risks, maximum development coverage and a maximum positive impact on the local community.

What are Development Incentives?

To resolve some of the main challenges of South African cities, in addition to planning documents, there are government incentives available to stimulate particular kinds of development. These include tax, regulatory, and other forms of help. New infrastructure and transport routes are also a form of incentive as they unlock land that was previously isolated. We consider these incentives together to decide what is the most relevant for our residential typologies. The Importance Verdict values are added to the resulting value of a site after it has been evaluated for Risks and Constraints (Fig.10 & 11).

For example,

- The site is located in the Dolomitic area and received a value of 0–3=-3 for Planning Constraints

- The Site is — at the same time — in the Transformation Zone, which has an Importance Value of 1 for Development Incentives

- The resulting combined value for planning constraints and development incentives is 0–3+1=-2.

Total of residential sites with the maximum number of incentives: 792

Step 7. Development Impact

Many cities are trying to promote more compact, mixed-use, walkable urban forms. Recent studies demonstrate many benefits of more compact and denser cities. For example, increasing building density by just 1% results in an 8.5% decrease in vehicle mileage. It reduces energy consumption by 7% and public spending by 14%. However, there are harms too. Higher densities contribute to the inflation of property prices and rent rates.

Johannesburg is on the same track — a large part of its planning arsenal aims to create dense nodes and equitable, walkable neighbourhoods. Nodal Review 2019/20 is one of the key and most recent policy pieces for the City of Johannesburg that promotes densification balanced with the provision of amenities and a transport system.

However, Nodal Review 2019/20 is a policy limited by the city boundaries of the City of Johannesburg. It is based on static data and does not include all social infrastructure and services.

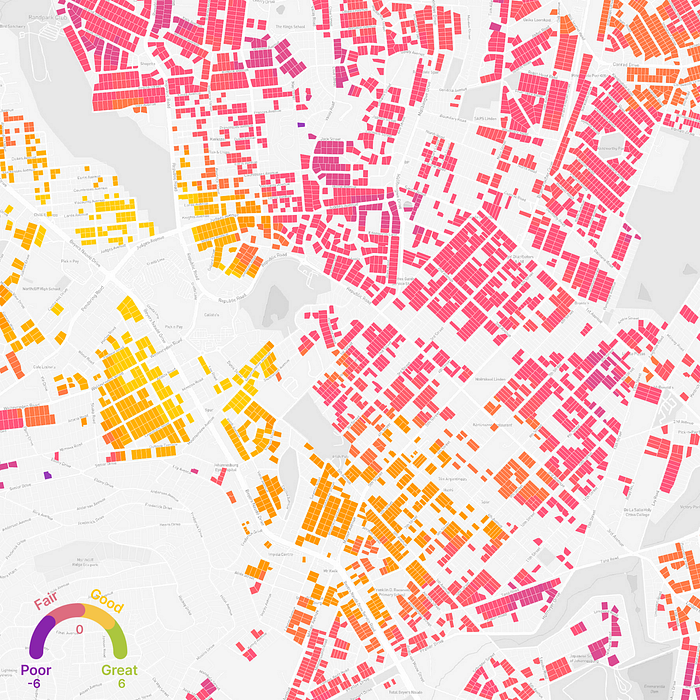

For this reason, we developed our indices: Public Transport Accessibility Index* and Local Amenities Index**. These indices demonstrate if development opportunity contributes to urban sprawl or compact and walkable urban structure. These indices are designed to scale nationwide and help property entrepreneurs see the real potential of a location nationwide and how this extra density is balanced with the provisions of transport and services.

* Public Transport Accessibility Index

As follows from the name, the index calculates the proximity to public transport routes and stops. If the development does not have access to public transport within walking distance it means that residents depend on cars and development contributes to urban sprawl. Depending on how many different modes of public transport are available a development opportunity gets a grade from — 6 to + 6. Negative values mean the development contributes to urban sprawl, while positive grades mean it makes the place more walkable and mixed-use.The following modes of transport are included in the calculation: Rea Vaya BRT, PRASA passenger rail, Gautrain train and Gautrain bus routes, Metrobus and taxi ranks. For each development opportunity, we searched for transit stops within a 15-minute walk. The more modes of transport are accessible the higher the grade. If there is no public transport stops accessible it means that the place is entirely car-dependent, and development opportunities get a grade of ‘-6’. If all available modes of public transport are available a site gets the highest grade of ‘+6’.

** Local Amenities Index

Local Amenities Index is similar to the Nodal Review calculation: it assesses how close a given area is to jobs and services. However, the Local Amenities Index has some differences. It contains more amenities, for example, retail, leisure, and sports facilities (Nodal Review accounts only for municipal infrastructure: public schools, parks, and transport). It uses real pedestrian networks to calculate an area accessible within 15 minutes on foot. In other words, the Local Amenities Index calculates an actual travel time and is a guarantee that residents will not need a car to get their groceries. One could think of it as a more advanced Nodal Review calculation that is more accurate, always up to date and available nationwide.In detail, for every address, the Local Amenities Index identifies how many amenities are available within a 15-minute walk. The location contributes to urban sprawl, getting a negative value if no services are available. The more services are available, the higher the grade is, and the more walkable and mixed-use the neighbourhood is.

We calculated the Local Amenities Index for each 250x250 meter cell of land. From every centre of a cell, we calculated a 15-minute walk area and counted all the commercial, educational, government and healthcare services.

Because services are of various priority, they are split into three groups and assigned distinct weights:

1) Necessary — services one needs daily, i.e. shops, pharmacies, schools, and child care. These services are essential for every family and are assigned a weight of 0.5.

2) Optional — services one uses when there is spare time (and money) — sports, leisure, going for a walk, eating out. Optional services are assigned a weight of 0.3. These amenities are indicators of a prosperous community.

3)Social — services one needs only occasionally: hospitals, post offices, and police stations. These services are pillars of a safe and inclusive community and are assigned a weight of 0.2.

Finally, we calculate Local Amenities Index as 0.5 x of Necessary + 0.3 X Optional + 0.2 X Social for every 15-minute walk area in any given location.

Negative values of the indices mean that the new project contributes to urban sprawl, while positive values mean an area will benefit from an extra density.

To get an instant measure for a new project we created Development Impact Gauge (Fig. 12) that combines two indices. The values of the gauge range from -6 for the worst impact to +6 for the projects with the best impact on the city and the community.

Step 8. Potential Development Coverage

At this stage, we use the calculations for potential development coverage (Fig. 13) to sort sites from the best to worst. The values are calculated in square meters and available on the OneCity Insights Report for Johannesburg.

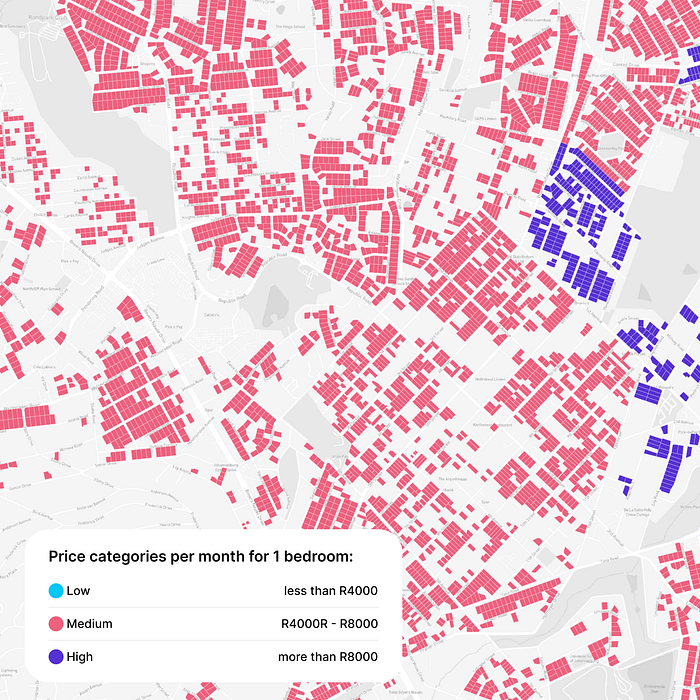

Step 9. Property Markets

The property rental market is an important benchmark to evaluate potential returns on investment. To account for it, we studied listings published on property marketplaces which provided us with current rental rates and their spatial distribution.

We analysed the spatial distribution of listings in Johannesburg by aggregating the prices by Main Places boundaries according to the latest Census. Each area has been categorised based on average rental prices per room within its boundaries. We used a total of 3 price categories: low, medium, and high. Low corresponds to less than R 4000 per month per bedroom, medium is R 4000–8000; high is more than R 8000 (Fig.14).

We ranged all plots against these price bounds and attributed each to one of the price categories. The price category for each land plot is provided in the OneCity Insights Report unless no data for the area is available.

Conclusions

In the current version of OneCity Insights, we identified 181 753 opportunities in Johannesburg to develop or extend single-family detached houses that fit the present property market climate (Fig. 15).

2 452, which is 1.5% of these opportunities, have high development potential and are close to amenities and public transport.

You can see the interactive map and find your development opportunities in Johannesburg by following the link:

City of Johannesburg CGIS, OSM:

- Land use rights

- Registration status

- Size

- Constraints

- Building footprints

- Public Transport

- Amenities

Microsoft Global ML Building Footprints:

- Building footprints

Property24, Remax, SAHometraders:

- Property markets